Federal Reserve Stress Scenarios Modeled In Riskostat

As you may know, the Federal Reserve recently released their stress scenarios: Base, Severe and Adverse. While the Fed may not explicitly regulate you, the role this organization plays in the financial markets cannot be underestimated. The specifics of their analysis are useful as the Fed has lots of up-to-date information at their disposal. But...Read More

What does Riskalyze ‘Risk Number’ really measure?

What does Riskalyze Risk Number really measure? Disclosure of calculation and methodology essential for meaningful discussion. Riskalyze has responded to our criticism of the math behind their interest rate stress test. Unfortunately, the response does not address a single point of substance and seems rather personal. Our systems serve some of the largest asset managers in...Read More

Crash Tests, Clairvoyants and Risk Managers

This blog entry is published in the Financial Advisor Magazine Expert Views Risk management is all about finding the suitable risk/return profile. Suitable, that is, to the holder of the portfolio. When your client has a suitable portfolio, he or she will not sell when the losses hit, because the possibility of those losses was...Read More

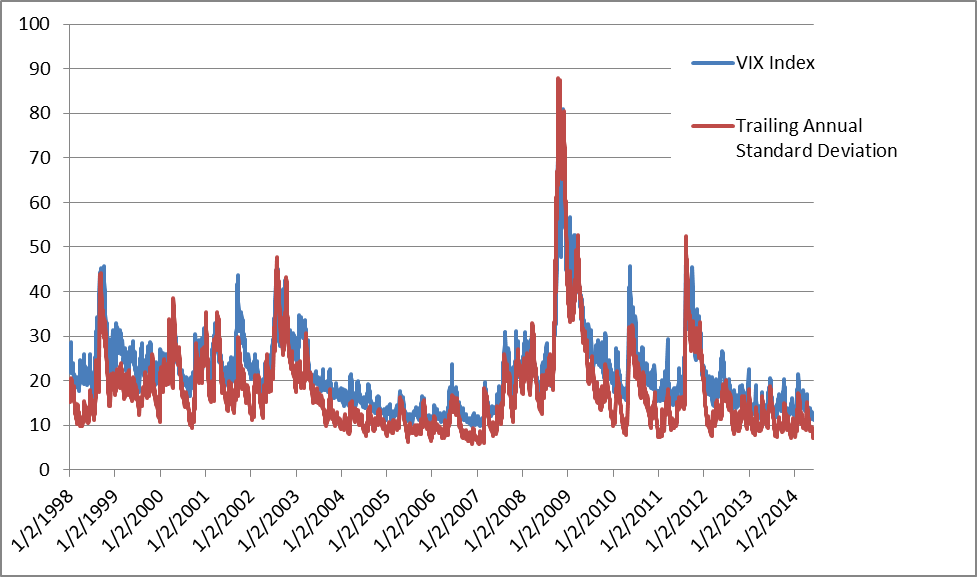

Black Swans Love a Low VIX

This RiXtrema blog entry is published in the Financial Advisor Magazine Expert Views As the VIX tumbles to lows not seen since before 2008, we must ponder the meaning of this complete disappearance of volatility. Are we really witnessing historically low levels of risk? Forward Looking Risk? VIX is supposed to be a measure of...Read More

What If Fed Tapers? How Does a Risk Manager Prepare?

In Part 2 the stress test of Fed tapering QE is discussed as a way to cover for shortcomings of risk models. Incorporating plausible macro scenarios is necessary to make risk models relevant again. RiXtrema researchers, a legendary risk manager Barry Schachter and RiXtrema President Daniel Satchkov participate.

Why Sharpe Ratio And Other Traditional Stats Can’t Prepare You For What’s Coming

Are you thinking about interest rate risk and how it might interact with equity risk? If you are using risk models, beware, they can be lying. We can improve the accuracy of the models by using portfolio stress testing, but we first must understand where their pitfalls lie. This post has a bit of a...Read More

Fund Crash Ratings for Wellesley, Wellington and Thornburg Income

Know your funds. Detailed comparison of risk profiles of Vanguard Wellseley (VWINX), Vanguard Wellington (VWELX) and Thornburg Investment Income Builder (TIBIX) funds. Which one is more sensitive to inflation or a financial crisis? What about Fed Tapers QE scenario? The funds are put through series of stress tests and the impacts are compared. Position level...Read More

Managing Interest Rate Risk For Wealth Management Clients

Majority of the investors are waking up to the fact that fixed income portfolios are not necessarily safest given historically low interest rates and the macroeconomic outlook. The video offers a way for financial advisors to quantify interest rate risk of any portfolio using RiXtrema’s Portfolio Crash Testing tool. Once the risk is quantified, an...Read More