Daniel Satchkov of Rixtrema believes advisers need to redefine their value to clients to compete with cheaper online advice offerings… Click Here To Watch Video

As you may know, the Federal Reserve recently released their stress scenarios: Base, Severe and Adverse. While the Fed may not explicitly regulate you, the role this organization plays in the financial markets cannot be underestimated. The specifics of their analysis are useful as the Fed has lots of up-to-date information at their disposal. But it may be even more important to consider what the Fed left out – either accidentally or intentionally. What the Fed Missed and What ECB Completely Ignored In many ways, these new Fed scenarios are an improvement over past variations. They are far more robust when it comes to the equity market shocks. For example,...Read More

What does Riskalyze Risk Number really measure? Disclosure of calculation and methodology essential for meaningful discussion. Riskalyze has responded to our criticism of the math behind their interest rate stress test. Unfortunately, the response does not address a single point of substance and seems rather personal. Our systems serve some of the largest asset managers in the world and top advisors in the US. We have published articles in scientific journals such as Journal of Risk Management in Financial Institutions, Journal of Asset Management and Journal of Risk Model Validation. In the world of scientific risk management, where we come from, it is completely acceptable to question math of competitors and...Read More

This blog entry is published in the Financial Advisor Magazine Expert Views Risk management is all about finding the suitable risk/return profile. Suitable, that is, to the holder of the portfolio. When your client has a suitable portfolio, he or she will not sell when the losses hit, because the possibility of those losses was discussed right from the beginning. The biggest problem for most investors is that they get in near the top and get out near the bottom. ‘Suitability’ ensures that this vicious circle is disrupted. But the only way that could happen if their risk/return tradeoff was chosen by considering a variety of scenarios: good, bad and ugly....Read More

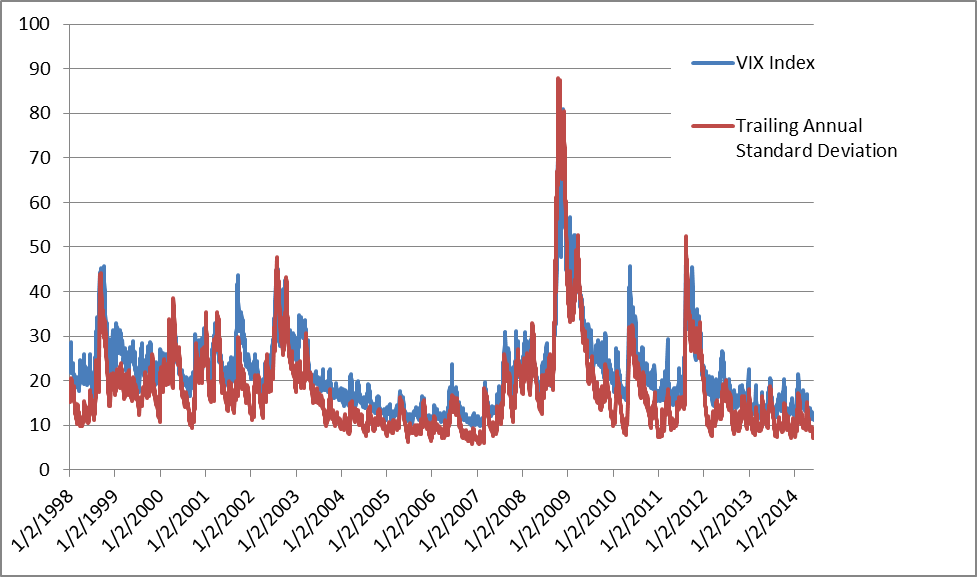

This RiXtrema blog entry is published in the Financial Advisor Magazine Expert Views As the VIX tumbles to lows not seen since before 2008, we must ponder the meaning of this complete disappearance of volatility. Are we really witnessing historically low levels of risk? Forward Looking Risk? VIX is supposed to be a measure of forward-looking volatility. It is based on decisions made by option traders from big investment houses with a lot of money on the line and that is quintessential “smart money,” isn’t it? In fact, their opinion of the future seems to look a lot like the recent past. Let’s consider the below chart, which shows VIX...Read More