Diversification by Twitter: How Trump’s Trade Tactics Are Changing Financial Markets

Donald Trump yesterday suddenly threatened to increase tariffs on many Chinese goods from 10% to 25% effective this Friday. He also threatened to institute many new tariffs. According to his math, the new tariffs will amount to 25% on about $375 Billion in goods or roughly $94 Billion per year. Chinese Communist Party is not yet used to bludgeoning by Twitter and Shanghai Stock is down 6% for the day. It was down by more, but rose after the intervention by the national stock market defense team. One can just sense the shock that Chinese authorities experienced from this tweet. In fact, mainland China press censored the tariff threat and this shows how vulnerable they feel.

Why was this threat such a shock to China and the rest of the global markets? Here is some background.

For close to three decades anyone analyzing the global economy had to assume greater and greater interconnectedness in global financial markets. Correlations between developing countries’ stock markets steadily increased, but more importantly correlations between developing markets like China and developed markets like the United States also increased.

There was a brief lull in those rising correlations in 2006-2007 when many analysts started talking about China decoupling from the US. The logic was that China became a significant force in the world economy in its own right and had its own gigantic internal markets. Plus some resilience in 2006-2007 showed that Chinese equities can hold their own to moderate volatility in the United States. As it was, the lull was short and the decoupling illusory. The fact that China could withstand minor jumps in US equity volatility did not mean that it could weather the storm. And when that storm came in the form of the Lehman Brothers bankruptcy, Chinese stocks dove much faster than even the nearly destroyed US banks.

The great decoupling of 2007 was a myth. And after 2008 crash when central banks of the world rushed monetary high to revive animal spirits, global markets yet again melted in one giant embrace. After 2008 financial markets became more and more interconnected to the point where central banks played more like a team than actual separate countries. Fed is pausing the stimulus, well, not to worry, let Mario Draghi and the ECB pick up the slack. Trouble in Europe? Let Bank of Japan print another trillion of something.

And then came the US-China trade negotiation. It seems to be the only real economic news since Lehman to seriously affect financial markets. For years, the only question on investors’ minds was ‘will they or won’t they?’, meaning, will there be MOAR stimulus. But US-China trading relationship is a lynchpin of the current global economy to such a degree that even Fed has to take a backseat. China is still the world’s pre-eminent producer and US the world’s consumer. China patiently recycles its profits from the trade with US into financial assets all over the world, all the while stimulating massive credit bubble internally. Financial markets around the world depend on Chinese money flows almost as much as they depend on dollar flows (some depend more).

Disruption in this producer-consumer-investor relationship is about to be upended.

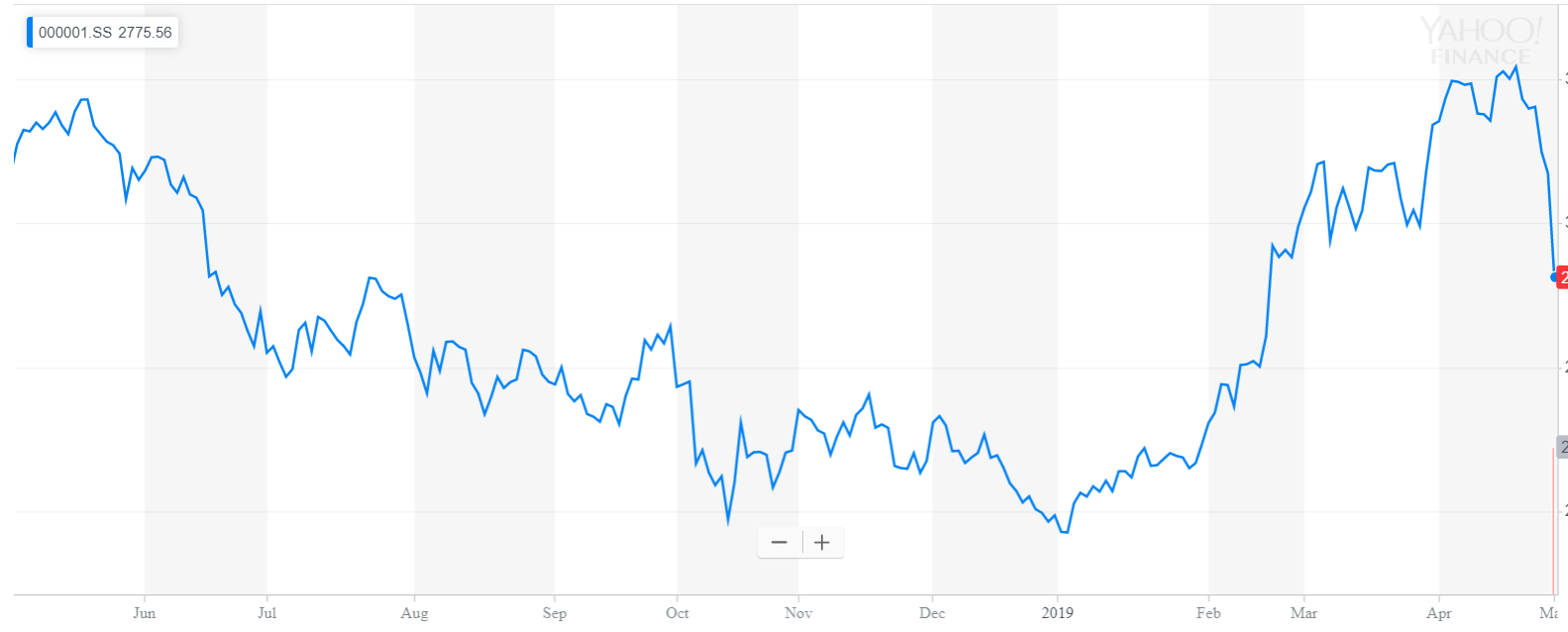

Markets still think that US-China deal will be settled and nothing major will change. If investors believed that the deal will actually change the relationship, there would be much more risk taken off the table in Chinese equities. I believe that most investors are complacent. If Donald Trump follows through on what he actually outlined as his preferred deal, we are not near the finish line. More so, by the time that deal is finally done, financial markets will decouple. And China will be much much worse off. While US markets will also suffer, in the long run they will hold much better than China. China depends on US for trade and for technology to a much larger degree than US depends on China. If you need to be convinced of that fact, consider just two pieces of evidence. First, let’s look at the Shanghai Stock Composite Index over the past year:

Note, that Shanghai Index lost nearly 30% through Jan 2019. Virtually all of that was due to worries about lack of hope for a kind of trade deal that would keep the current setup more or less intact with some moderate concessions.

It was around Jan 2019 when hopes for trade deal started to rise again and along with Fed’s newfound dovishness this propelled Chinese stocks upward. But those hopes are dashed once again and market duly obeys.

China depends on US both in terms of trade flows and actual technology used in production of goods. To be convinced that China still depends on US for technology, consider the case of ZTE, Chinese telecom giant. When US banned sales of US products or technology to ZTE in 2018, ZTE announced shutdown of operations in mere days. So swift was its destruction, you could be forgiven to think that ZTE is some small or regional business that was critically dependent on one or the other component from the US. If that were so, they could try and go to Europe or Japan. But ZTE was one of largest Chinese companies, second largest telecom company in China behind Huawei. Here is a short of list of component supplies that they lost in that ban: “For all of the types of equipment it makes, ZTE needs many critical hardware and software components made by U.S. firms including processors, memory, optics, antennas, screens, operating system or applications from the likes of Google, Intel, Micron, Qualcomm and many more.” (Source)

US can easily redirect most consumption to purchase goods from other countries e.g. Vietnam. For China, there is no other market like US and they have not developed their internal market enough to make a difference. If Trump administration keeps ramping up pressure to essentially redistribute global trade, China will be the main loser. The effect on the equity markets will be negative across the globe, but in the US it will be more muted relative to China. And when turmoil stops, US will be on a much more solid footing economically. And if administration does follow through on its threats and makes a game-changing deal (as opposed to cosmetic makeover), US and China equity markets may very well decouple, but not for the reason that pundits foresaw in 2007.

There is an apocryphal old Chinese curse that goes like this: “May you live in interesting times”. In fact, there is no such Chinese saying, but it does illustrate some cliches many have about Asia. But be that as it may, we are living those times now. And Chinese authorities and investors in Chinese assets sure should hope for things to get less interesting very very fast and for Trump administration to walk back on these comments.

Cover Image Source: http://kidskunst.info/linked/donald-trumps-10-most-offensive-tweets-forbescom-646f6e616c64.htm

Read the Latest Case Study from Larkspur-RiXtrema: What will Happen to my Client’s Portfolio if the Chinese Credit Market were to Explode?