How to Create Tremendous Savings For Plan Participants Without Reducing Your Fees

ERISA based litigation is exploding. Targets of litigation include both large and medium sized plans. Legal challenges against Anthem, Boeing, Lockheed Martin, International Paper, MassMutual & Ameriprise are only some of the examples. Incentives to litigate are extremely high due to significant attorneys’ fees awards.

Investment management fees on plan assets represent up to 80% of a 401k plan expense. To help plan sponsors and financial advisors reduce participant costs RiXtrema released ‘401kFiduciaryOptimizer’, a software that analyzes investment fees of funds offered in the plan. ‘401kFiduciaryOptimizer’ uses sophisticated quantitative techniques to identify alternative investments that could save the plan participants significant amount of money. The alternatives offered are very close matches in terms of risk/return profile to the assets in the plan, but with lower expense. Advisors can create proposals that offer significant savings to plan sponsors.

I. Introduction: New Tobacco?

A recent ruling by the Supreme Court in Tibble vs Edison stated that plan fiduciaries have ‘a continuous duty’ to monitor mutual funds in the 401(k) accounts for unnecessarily high fees. This ruling effectively shifts burden in disputes from workers to fiduciaries that administer the plans. More so, a flood of new lawsuits is expected because recent rulings have awarded significant attorney fees, thus incentivizing lawsuits . Here are some examples:

- In Tussey v. ABB, Inc. award was $11.6 million in attorneys’ fees

- Both Novant Health and Boeing agreed to settle fee-related suits for $32 million and $57 million, respectively

- In Haddock v. Nationwide Financial Services, Inc attorneys fees awarded were than $50 million

- In Krueger v. Ameriprise received final approval of a $27.5 million settlement with $9.2 million in attorneys’ fees

New suits targeting Anthem, Insperity and Oracle have been filed even more recently. Mid-sized and smaller plans are also under attack as major rulings pave the wave for tobacco-like flood of litigation.

II. 401kFiduciaryOptimizer Software

401kFiduciaryOptimizer software is produced by RiXtrema, a leading investment risk management and research platform. Key features of 401kFO address some of the main responsibilities of an ERISA fiduciary in the area of investment expense and diversification. We will focus on mutual fund expenses in this paper. Here is how 401kFO helps reduce participants’ investment costs:

- Find Best Fund Alternatives With Lower Expense. Quantitatively analyze funds that are available in the plan and compare their risk/return profile to a universe of mutual funds available to the plan

- Calculate Potential Savings To The Plan. Calculate $ cost savings for the plan participants from switching to lower cost alternatives

- Check For Adequate Diversification. Quantitatively analyze available fund options to ascertain the degree of diversification these options provide e.g. are there certain risk-return profiles missing from the plan selection?

- Monitor Performance. Monitor performance of fund investments and fund watchlist

Every estimate is based on transparent algorithms with strong foundation in scientific literature.

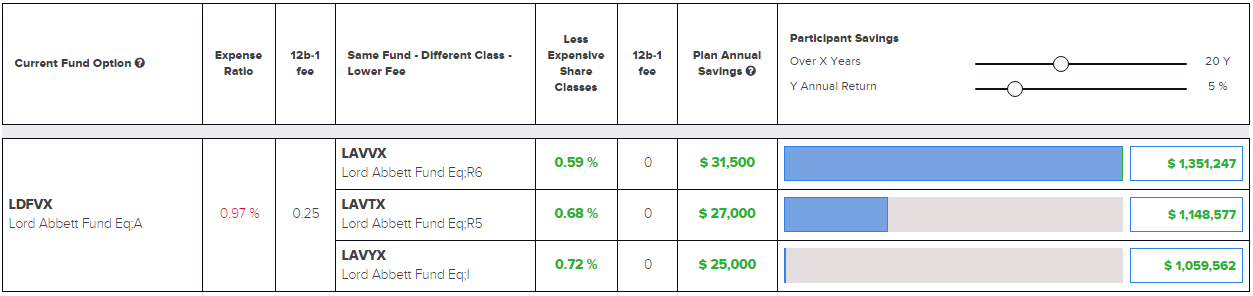

Let’s look at an example of how one plan can save millions of dollars with 401kFO. Plan XYZ has a number of funds offered to the participants. We will consider one of the funds, Lord Abbett Fundamental Equity Class A (LDFVX). This particular fund has an expense ratio of .97% and additional 12b-1 fee of .25%.

III. Same Fund – Different Share Class – Lower Fee

Firstly, before even we get to sophisticated quantitative algorithms, we should note that this fund has less expensive share classes available for plan participants. In exhibit 1 we show the alternative share classes for this fund, specifically the Institutional class (LAVYX) with expense ratio .72% and no 12b-1 fee, plus R5 & R6 classes (LAVTX, LAVVX) with expense ratios of .68% and .59% respectively. Assuming that participants invest $5,000,000 in this fund and that it returns 5% a year, the savings from switching to R6 share class would amount to $1,351,246 over a 20 year period.

Exhibit 1 – Lower Fee Share Class Replacements For LDFVX

This is just one fund available to participants and we are switching over to an identical fund. The fund we are replacing this way need not necessarily be a high fee fund. In fact, a recent lawsuit filed against Anthem Inc. targets precisely this type of problem. The suit focuses on some Vanguard funds chosen by the plan fiduciary, where a cheaper class was available. The fund targeted in that lawsuit has what seems like relatively benign expense ratio of .16%, but an even cheaper share class was available for .09%, so a potential fiduciary liability was created.

IV. Looking For Bigger Savings For Plan Participants

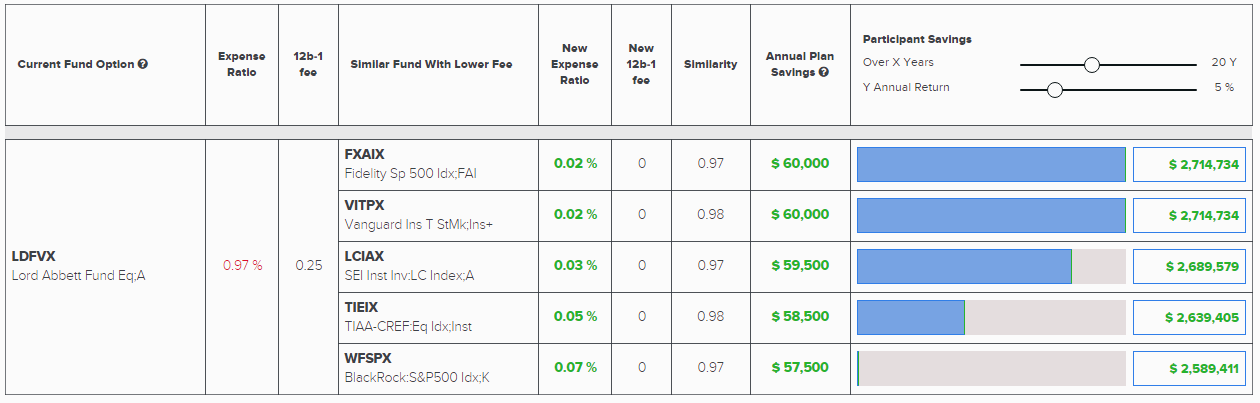

With all of the regulatory changes, it is certain that plan sponsors and RIAs that serve them will have to reduce fund costs significantly from where they are now. Otherwise they will be targeted for regulatory scrutiny and possibly litigation. Switching to another available share class with lower fees is a no-brainer and those who do not do it are opening themselves for litigation. However, plan fiduciaries could go further and incorporate a more rigorous search for cost savings into their process. 401kFO uses cutting edge quantitative modeling methods based on Modern Portfolio Theory and beyond to enable fiduciaries to do just that. Details of the algorithm can be found in Appendices A, B, C. It is based on established science and research from a highly respected group of risk managers . Let’s take our Plan XYZ and the same Lord Abbett Fundamental Equity Fund. After running 401kFO software we can see that there are number of very similar significantly lower fee funds that could be used as replacements (see Exhibit 2).

There is the Fidelity Spartan S&P 500 Index Advantage Fund (FXAIX) with an expense ratio of .025%! Similarity or average correlation of FXAIX with Lord Abbett (LDFVX) that is currently in the plan is .97, which is extremely high. To appreciate the significance of .97 correlation, consider the fact that correlation between S&P 500 and Dow Jones Industrials, two widely used measures of stock prices, is only .9! Utilizing the statistically similar FXAIX would result in savings of $2,702,151 over a 20 year period and same assumptions as above. In other words, if return exceeds relatively muted 5%, then participants will save more than half of their original investment over a 20 year horizon. And this is only one fund.

Exhibit 2 – Statistically Equivalent Lower Fee Funds

To confirm visually the similarity between the funds offered as alternative, RiXtrema’s 401kFO tool shows a graph (see Exhibit 3) comparing performance of the plan fund with alternative. Note how closely all of the funds from Exhibit 2 move together.

Exhibit 3 – Performance of LDFVX & Statistically Equivalent Lower Fee Funds

In fact, FXAIX (red line) has even done slightly better than LDFVX (blue line) over the 3 and 5 year period and it is a fund that could save millions for plan participants. In short, very significant savings are available to plan sponsors who are willing to utilize sophisticated methods of fund comparison in their process. Courts have ruled that plan fiduciaries have a «continuing duty to monitor» investments in the plan and 401kFiduciaryOptimizer is a very effective to fulfill that duty, while reducing plan participants costs in a big way.