- A Lookback at the Market Reactions During SARS

- Coronavirus Vs SARS

- Finally, the Reason You Started Reading This Blog Post

We have written a lot about the potential for market corrections and scenarios that may disrupt the decade long bull market. The Coronavirus is the most tangible example of a short-term threat to the market’s long upward climb. And our clients, keenly aware of the potential for market disruption, have asked us to create a Coronavirus stress scenario for Portfolio Crash Testing Pro. Many have also asked us to load a SARS scenario as a proxy for a Coronavirus style stress test. For reasons that I will review below, there are many differences between Coronavirus and SARS, and thus a comparison to SARS may be inadequate.

A Lookback at the Market Reactions During SARS

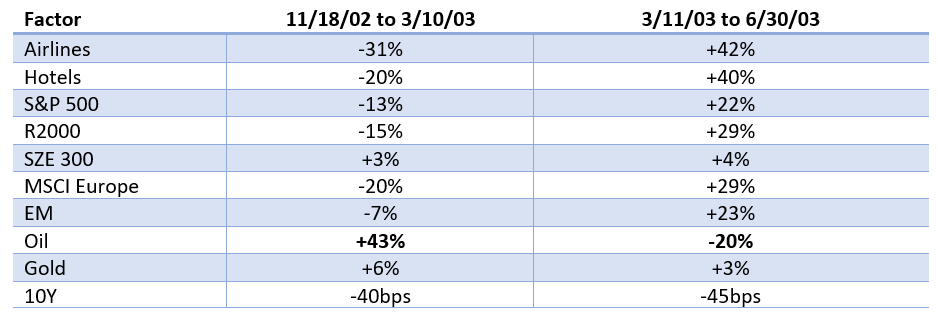

First, let’s take a quick look at SARS. According to the World Health Organization (WHO), SARS was first reported on November 16, 2002. WHO issued a global alert for SARS on March 12, 2003, and gave the all-clear for different countries between May 6 and July 3, 2003. The market sell off in the US corresponds more to what I would expect, and that is a sell-off reaction to the early confirmed cases of SARS, with the rebound starting shortly after WHO acknowledged a problem, a period of roughly 4 months. Over that period, here are some market reactions (taken roughly from peak to trough and trough to June end, all in USD):

Oil reacted more to the travel bans/warnings enacted during SARS, not the spread of the disease. Gold also had a much more substantial spike to January (+20%), which may have been peak panic but retraced to March. What is really interesting to me is that ground zero for SARS, in China, the Shenzhen 300 was up in both periods.

Coronavirus Vs SARS

But all this may be noise, as it is a bit difficult to draw parallels between SARS and Coronavirus for a few reasons. First, markets were already depressed when SARS hit. The first official case was reported about 45 days after the Tech bubble bottom. SARS may have delayed the bounce, but the effect on US Equity was relatively benign. China stocks were positive (depending on the dates used, so were US stocks). Clearly the markets aren’t depressed in 2020 and would have more room and reason to fall from highs, but…

The response from China is much stronger this time. They have sacrificed the Wuhan province to stop the disease spread. If they could put a bubble over Wuhan, they might even do that. But this gives markets more confidence that the effect on the global economy will be somewhat limited. With SARS, it took 4 months for the WHO to issue an official alert. They have already issued a formal warning here and took less than a month to do so. Apparently, they have learned from SARS, Ebola, and MERS. These actions will likely give market participants some confidence. That confidence is important since Coronavirus has the potential to be much more devastating, given the rapid spread and number of fatalities in such a short time. Still, I think governments are doing a fine job convincing citizens that they have the situation under control.

The decline in yields is different. 10Y rates at 4% after a market correction and a fed cutting rates to kickstart an economy is different than rates at 1.7%-ish and today’s Fed’s super accommodative, let the bull run at all costs approach. So the flight to safety option will be somewhat compromised, especially in the Euro region where rates are much lower (generally). But there is always the possibility of 0% and lower yields on the US 10 year.

Finally, I think investors have some experience dealing with the relatively short time frame and isolated effects of these global pandemics. We have had SARS, MERS, H1N1, Ebola, and now Coronavirus in the last 18 years, and I think that people just think it will be like SARS again (we have been asked by MANY clients to create a pandemic scenario like SARS too). But, if people expect this is just SARS all over again, then the global economy should not worry about much more than some minor disruptions.

Assuming that the pandemic will turn out ok ignores the ugly truth about the virus – it is spreading far faster than SARS ever did and in a shorter time-period. According to WHO, SARS had 8,096 reported cases, with a resulting 774 probable deaths over 19 countries. In about 4 weeks, Coronavirus has reported 40,000+ cases, almost 5000 of them are ‘critical’ and 900 deaths so far. That’s a lot of numbers, so see the summary table below.

*Table updated on Feb 12, 2020, latest Coronavirus statistics here.

Coronavirus has had over 5x the number reported cases compared to SARS in a fraction of the time and more fatalities. The saving grace is that the percentage of fatalities is much smaller than we saw for SARS, but that can quickly change as time passes. The number of deaths as a percentage of resolved cases is very high.

But to put this in perspective, in the US alone, the CDC reports that there have been a reported 19 million Influenza cases (through January 15, 2020, the latest data available as of this writing) with 10,000 deaths. From the report, “Based on these figures, severity is not considered high at this point in the flu season”.

The critical difference lies in the mortality rate of the contagions, with SARS being the highest by far of recent pandemics. There is also the unknown regarding exactly what Coronavirus is. The flu is well understood and accepted as a normal part of life. Coronavirus is a mystery to most, and the name alone has caused confusion. My favorite lighthearted headline regarding the virus this far is from the Wall Street Journal: “Your Corona Is Safe From Coronaviruses – No Need to Add Disinfectant”.

Finally, the Reason You Started Reading This Blog Post

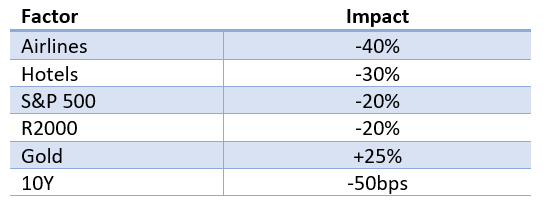

Ok, back to stress testing. Given all these caveats, I created a stress test for use in Portfolio Crash Testing that assumes an escalation in reported cases, mortality rate, and geographic spread of Coronavirus.

Geography is particularly essential, in my opinion. Wuhan province is similar in population to New York City but spread over a much greater area. So, if the reported cases and mortality rate increase only in Wuhan province, then the global economic effects will be limited. In fact it may even be in the past (remember the down week in January – that’s likely the impact in the Wuhan only scenario). Wuhan is not New York. But effects will be more pronounced if the virus spread in Wuhan is mirrored in a place like New York as opposed to the Philippines, for example. Even a more widespread outbreak in China could be very disruptive to the global economy given the proportion of global GDP from China relative to 2003.

Here are my factor impacts.

Coronavirus Pandemic Stress Test

I also caution that if a downturn begins with the spread of the Coronavirus, then I would not expect as rapid of a snapback as seen during SARS. With a 10 year bull market in the rearview, potential for profit-taking, summer on the horizon, and a US election season upcoming, along with some mixed economic data, not to mention the depleted resources of global central banks to come to the rescue, a Coronavirus related sell off could interrupt the bulls for an extended period.

And remember, our new RegBI Optimizer tool has a built-in version of Portfolio Crash Testing (PCT). PCT enables users to conduct a rigorous analysis of suitability when doing a rollover for a client. And when doing a rollover for a qualified plan, RegBI Optimizer is the only tool that can include metrics such as Plan fees, red flags, and holdings (for audited Plans) alongside risk metrics to ensure complete analysis. So you can add an up to date scenario like the Pandemic Stress Test to show clients and prospects that you have their best interest in mind when doing a rollover.