According to the recent Blackrock Investor Pulse Survey, we are in a retirement crisis and advisors who work with pre-retirees are on the front lines. Investors are generally pessimistic about investing. The survey indicates that 72% of Americans do not see financial markets as a way to put money toward their long-term goals, which is disconcerting for financial advisors. Retail investors have been pulling money out of both stock and bond funds for the first time since the 2008 crisis – and the same underlying dynamic is at play. People feel like there is too much risk in the markets for them to participate.

Even people that actively invest money have negative feelings about investing – 49% of current investors harbor such feelings according to the Blackrock survey. It seems that they are investing because they see that investing is the only way to get to their goals, but will they have the stomach to stay in the volatile markets? This is a bleak picture and only advisors who have a very solid value proposition and a risk management strategy will be able to address these client emotions.

Paradoxically, 84% of Americans expect to be free to pursue their interests and hobbies, 77% expect to travel as they wish and 74% expect to feel financially secure. How does one explain this? After all, investing in a growing and stable market is the only thing that can give them such a secure retirement, yet at the present time they feel that the risks are too great.

But while expectations are lofty, retirement reality bites. The average investor saved $136,200 for retirement, but will need $45,000 annually to meet their retirement expectations. How are they going to generate that? $136,200 savings will yield only about $9K per year, or 20% of their required income and even that with fairly benign assumptions.

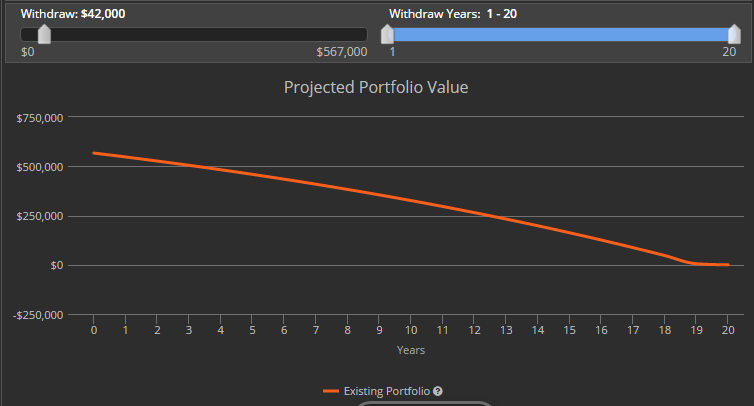

The same issue affects affluent retirees. They’ve saved an average of $567,000, but need close to $60K per year to meet their desired lifestyle costs. They cannot possibly get that. Consider Exhibit 1. Let’s say that our affluent investor has a portfolio that yields 6.3% a year (which means it has significant equity and corporate debt exposure). Further, let’s assume that the retirement period is only 20 years and that there are no market crashes of any sort throughout the 20 year period (a truly optimistic assumption). If this affluent investor attempts to withdraw only $42,000 per year in real terms (keeping the purchasing power), he or she will run out of money in year 19 even in this most rosy scenario.

Exhibit 1 – Investor saved $567,000, wants $59,600 per year, but can only get <$42,000 in best case

Source: Portfolio Crash Testing, www.rixtrema.com

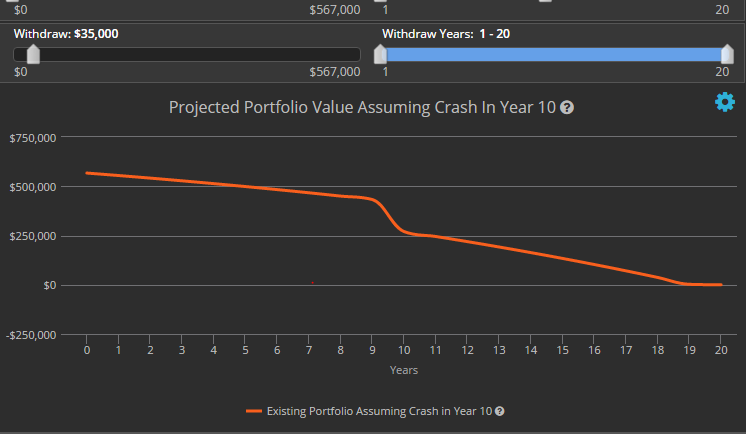

What if there is a significant market crisis in the middle of the retirement (10 years from now). Check out Exhibit 2. In this more realistic scenario that portfolio could only support $35K withdrawal and even then, it will run out of money in year 19.

Exhibit 2 – Investor saved $567,000, wants $59,600 per year, but can only get <$35,000 in realistic case

Source: Portfolio Crash Testing, www.rixtrema.com

But all this is still too optimistic. Why? Because we assumed that the retiree has a growth portfolio and markets behave reasonably well (no crises or only one crisis in the next 20 years). In reality, Blackrock’s survey finds that 65% of the wealth of those individuals is sitting in cash! At the same time, 57% believe that their investments are diversified enough to help reach their goals.

What’s an advisor to do?

First and foremost, advisors need to ensure that their clients’ expectations are based in reality. Frequently investors’ have unrealistic expectations and advisors must address this.

Secondly, advisors must explain to investors that holding cash is not a viable long-term strategy (though in a period of very high uncertainty it could be quite reasonable). But in order to talk about portfolio management credibly, advisors must offer a viable risk management framework. Holding cash is the only risk management strategy investors now understand, so advisors need to become risk management experts to offer alternatives. Unfortunately, the Fed’s zero interest rate policy made safe yield an endangered species, so investors will need better risk protection than simply buying some bonds. Significant amount of Treasuries, some put options, tactical funds all need to be utilized with the understanding that while any single strategy could fail, at least some of them would work to cushion the blow.