Your 1 minute case study on 401K Retirement Plans: A Rollover to an IRA Account

Regardless if your clients are plan sponsors or individuals who invest in their retirement accounts, as the advisor you can be a great fiduciary by helping them to achieve their goals. You can accomplish this by diligently reviewing plan options, finding a more affordable plan administrator, screening for the best investment funds that will suit the participants or advise on the rollover, you as the advisor should have all necessary information to act in the best interest and to be a good fiduciary for your client.

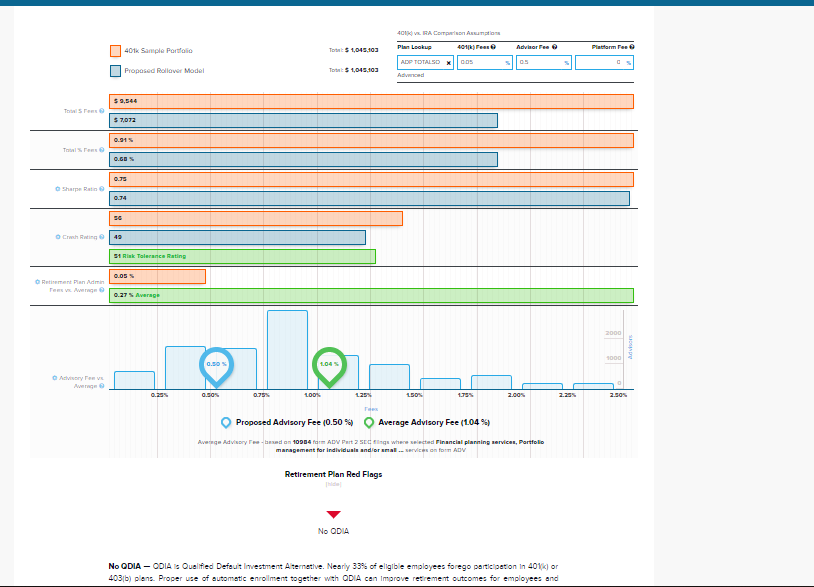

For example, if you are advising an individual who wants to rollover from a 401k plan to an IRA account, you can help them to see the benefit of such a move by comparing various fees like the admin fee vs. advisory fee, advisory fee vs. benchmark advisory fee, risk of investment vs. risk tolerance. The screenshot below illustrates that a rollover from a qualified plan to an IRA account is a good move for the participant because it reduces the cost of the retirement account to 68 bps (advisory fee of 50 bps and the cost of funds 18 bps) from 91 bps (admin fee of 5 bps and the cost of funds 86 bps). Also, the suggested rollover portfolio is better built to meet the client’s risk tolerance, which is very important, since risk management is the integral part of the retirement planning.

With the IRA Fiduciary Optimizer, the rollover becomes a guided step by step process which helps to facilitate and illustrate the rollover. More importantly, it helps to document the entire process to satisfy any compliance rules and to fulfill your role as a fiduciary. Detailed illustrations and diligent risk/financial planning questions will bring the best fiduciary practices to life. Advisors who follow the fiduciary rule would earn the respect and money of their clients because they prove themselves to be advocates of the best interest of their clients while using the best tools available to them.

See our other case studies or schedule your personalized tour of IRA Fiduciary Optimizer today:

Pingback : WHICH FINRA REGULATIONS ARE PART OF THE DOL RULE BEST INTEREST REPORT REQUIREMENTS?