Case Study: What will Happen to my Client’s Portfolio if the Chinese Credit Market were to Explode?

The Ask:

It is a fiduciary duty of each advisor to protect investments of a client. How can it be done effectively before a disaster strikes? It is customary to think about portfolio protection strategies when dealing with events close to home, such as a looming economic recession and market correction. You know the portfolio, so you can take measures to reduce the exposure to such events. What if the event which is about to happen is not so well known to you? How can you correlate events far from home to your portfolio and come up with an effective strategy to mitigate investment risk?

The Problem:

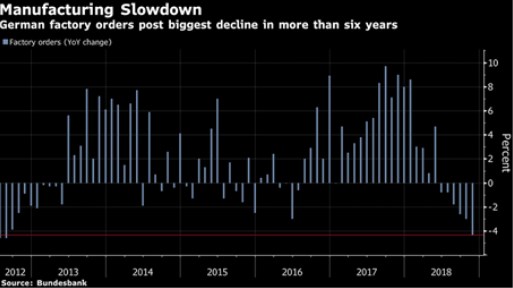

If you know about the developing problem with the Chinese credit market, how can this knowledge be used to prepare your client’s portfolio to withstand such an event? Recently, Bloomberg News mentioned another default by two large Chinese borrowers. These events continue to point out the vulnerability of the Chinese economy bloated on government debt. The explosion of the Chinese credit market will reverberate throughout the global economy. Especially now, when other major economies are about to nose dive. Take a look at the German manufacturing sector slowdown (see figure below) or US retail sales experiencing the biggest drop in nine years last in December. Such events are just some of the examples of possible recession indicators from the largest economies in the world. With no clear sign who can drive the global economic engine forward, sputtering of the Chinese economy will, no doubt, affect everyone else.

The Solution:

Portfolio Crash Testing (PCT) is a stress testing tool developed by RiXtrema based on its Riskostat software used by large asset managers. It enables financial professionals to understand how their portfolios are likely to behave in a variety of macroeconomic scenarios. PCT is based on a factor risk model. Every security has unique betas to a set of factors that explain its behavior. Any given equity will be exposed to local market beta, global market beta, variables such as growth, value, size, liquidity, oil price, industries, etc. A bond will be exposed to different points on a yield curve and to appropriate spread factors.

Stress test portfolio return is a weighted sum of individual security simulated returns. For example, the hypothetical portfolio stressed by “China Corporate Debt Explode” scenario shows the loss of 23.9%. On the right side of the screenshot, there are positive and negative contributors to the scenario. This information can be used to create a contingency plan on how to reduce exposure to this possible event. Be sure to read more on the risk management and request a personalized demo of PCT here or by clicking on the banner below.

Pingback : Diversification by Twitter: How Trump's Trade Tactics Are Changing Financial Markets